The Bottom Line

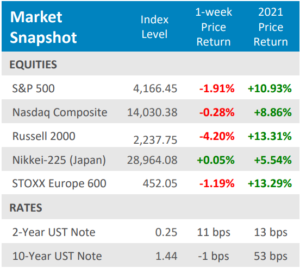

- Equities finished another volatile week solidly lower, with the S&P 500 dropping ‐1.9%. After leading large caps for three consecutive weeks, the small cap Russell 2000 fell sharply, losing ‐4.2% for the week.

- The yield on the 10‐year U.S. Treasury was little changed, down‐1 basis point, but that masked some big swings in the bond market. Following a surprisingly hawkish tone by the Fed, short yields doubled and long yields fell.

- Homebuilder confidence remains historically high, but it has been dropping lately and now building permits are falling too. Meanwhile May retail sales were softer than expected and unemployment claims unexpectedly rose.

Stocks battered, yield curve flatter

Global equities finished another volatile week solidly lower, as the U.S. Federal Reserve surprised markets by forecasting earlier‐than‐expected rate hikes and indicated it will discuss tapering asset purchases in coming meetings. The Federal Open Market Committee (FOMC) is now forecasting that it will hike rates twice in 2023 after previously predicting no hikes until 2024. Comments from St. Louis Fed President James Bullard—a non‐voting member this year—added to the Fed’s hawkish tenor with his comments Friday morning. The so called “reflation trade”, which favored value stocks and commodities, came under immediate pressure following the FOMC shift. The bond market also saw significant swings this week as the Treasury yield curve flattened noticeably, with the yield on the 2‐year note almost doubling and longer‐term yields, such as the 30‐year bond, falling (the 30‐ year US Treasury yield plunged ‐16 basis points on Thursday alone). The U.S. Dollar Index rallied to levels not seen since April. Economic data didn’t help as May retail sales came in softer than expected, manufacturing growth in New York and Philadelphia slowed, jobless claims snapped a string of weekly declines, and producer inflation ran hot.

Digits & Did You Knows

SLIGHTLY USED — The average age of vehicles on U.S. roads last year was 12.1 years, a record high. The average has been rising steadily for 15 years as car quality has improved, but the pandemic accelerated the trend (source: Dow Jones).

LEAVING TOWN — Between 7/01/19 and 6/30/20, 5 of the 10 largest cities in the U.S. saw their populations decline – New York City, Los Angeles, Chicago, Philadelphia and San Jose (source: Census Bureau, BTN Research).

SPENDING — Americans imported $278 billion of foreign goods and services in March 2021 and $274 billion of imports in April 2021, the 2 highest months in U.S. history (source: Bureau of Econ. Analysis, BTN Research).

Click here to see the full review.

—

Source: Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange‐traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds may be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐YieldBond(iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 ValueETF);MidGrowth(iSharesRussell Mid-CapGrowthETF);MidValue (iSharesRussell Mid‐Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory services offered through Prime Capital Investment Advisors, LLC. (“PCIA”), a Registered Investment Adviser. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).

© 2021 Prime Capital Investment Advisors, 6201 College Blvd., 7th Floor, Overland Park, KS 66211.

- Markets are ‘aimless’ amid rate cut uncertainty: Strategist - April 15, 2024

- Prime Capital Investment Advisors Named Finalist For RIA Of The Year - April 12, 2024

- KCBJ reveals 2024 Champions of Business honorees - April 10, 2024