Quick Takes

- A Comeback for Equities. The stock market did not like the start of August, but the indices ended the month higher after early declines. The first week of August saw the S&P 500 decline by over 4% and the Nasdaq decline over 5%. Both indices ended the month higher though finishing up over 3.5% each.

- The Road to 2%. As interest rates remain high and the labor market normalizes, inflation continues to decline. In July, the Consumer Price Index (CPI) fell to 2.9%. Meanwhile, the Fed’s preferred inflation gage, the Core Personal Consumption Expenditure (PCE) Index fell slightly from 2.8% to 2.7%.

- Dollar Declines Continue. As potential Fed rate cuts in September remain in focus while other central banks around the world are holding rates where they are or are raising them, the U.S. dollar continues to slip. The Bank of Japan raised rates at the end of July and August saw Fed Chair Powell change his tune on interest rate cuts for the first time since 2022.

- Income and Jobs. The U.S. saw unemployment rise in July as job creation slowed. Unemployment rose to 4.3% from 4.1% as the change in nonfarm payrolls came in at 114k, below the expected 175k and much lower than the previous month’s level of 206k.

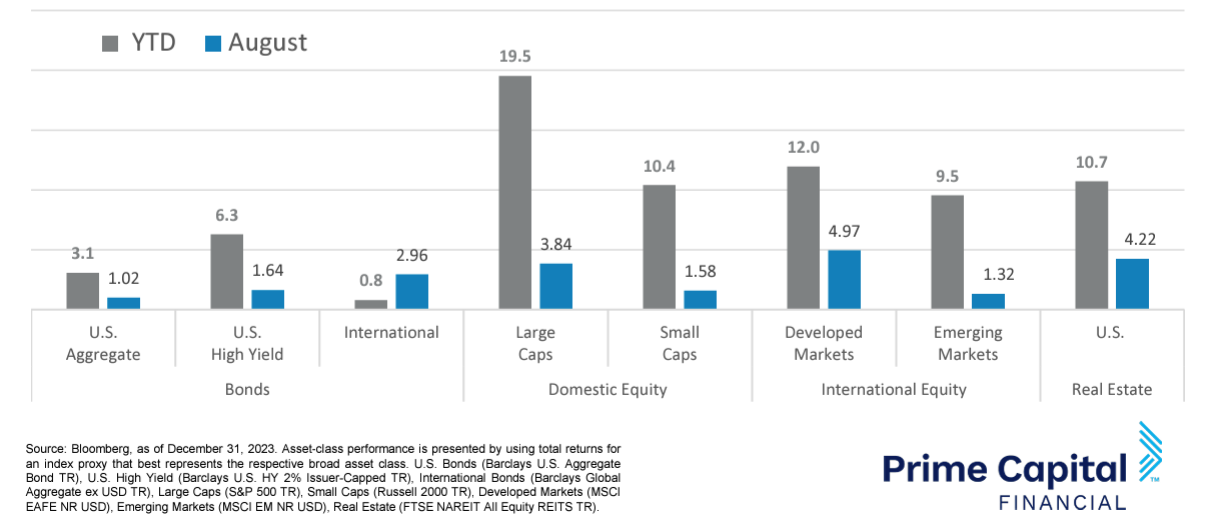

Asset Class Performance

Large Caps had a strong August relative to Small Caps, reversing last month’s pattern. Developed International equities outperformed the U.S. market during the month amid both actual and anticipated changes in monetary policy. Asset classes across the board saw gains in the month of August including both fixed-income and equities.

Markets & Macroeconomics

With institutional investors unwinding their positions in the Yen carry trade at the beginning of August, large U.S. technology stocks dragged the indexes lower in the first week of the month. This trade involved borrowing in Japanese Yen at low interest rates because of the Bank of Japan’s ultraloose monetary policy and using the borrowed funds to buy U.S. technology stocks, especially AI highfliers like Nvidia, Microsoft, and Google. This trade became less attractive after the Bank of Japan raised interest rates at the end of July and interest rate cuts by the U.S. Federal Reserve seemed increasingly likely amid weakening jobs data. As a result, institutional investors began selling their U.S. stock holdings to buy Yen and repay their borrowings. This led to a rocky first week of August for stock markets globally. Among the U.S. indices, the S&P 500 declined by over 4% while the Nasdaq declined by over 5%. Nvidia, Microsoft, and Alphabet were among the largest underperformers in the S&P 500 falling 9.5%, 4.5%, and 6.8% respectively. In the second half of August, weak economic data, investor concerns about the return potential on substantial AI-related capital expenditure, and stretched valuations hit mega-cap technology stocks again. As companies reported their quarterly earnings results, analysts increasingly scrutinized the amount companies were investing in AI and the productivity gains that would result. This, combined with elevated investor expectations, resulted in strong earnings results and guidance raises by Nvidia failing to lift stocks. In the second half of August, Nvidia declined by nearly 3% even after reporting better than expected earnings and revenue and raising their forecasts for the current fiscal year. Meanwhile, stocks in sectors like consumer staples and health care outperformed the S&P 500 and the Nasdaq in the second half of August with Walmart especially performing well after earnings.

Bottom Line: With price pressures easing, the labor market loosening, stock valuations high, and stock market indices concentrated in high-growth, mega-cap technology stocks, investors have become more cautious. The high valuations of large technology companies started to moderate in August as investors reset their expectations around companies’ ability to outperform analysts’ forecasts going forward. Optimism about interest rate cuts have been reinforced by Fed commentary. Investors are also looking to sectors beyond technology which have seen less of an increase in valuations over the last 18 to 24 months for new opportunities and diversification. Rate cuts and sector performance will continue to be in focus in September.

Download the full review.

©2024 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Sources for this market commentary derived from Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Financial | Wealth | Retirement | Wellness. Securities offered by Registered Representatives through Private Client Services. Member FINRA/SIPC.

© 2024 Prime Capital Financial, 6201 College Blvd., Suite #150, Overland Park, KS 66211.

- Expect market to rally at end of 2024, says strategist - September 11, 2024

- Month-in-Review: August 2024 - September 10, 2024

- How Financial Advisors Use Office Decor to Break the Ice - September 6, 2024