The Bottom Line

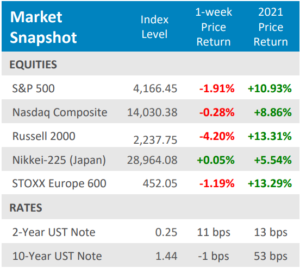

● U.S. equities reached more record highs after seven straight gains, it best winning streak in 10 months. It was the second straight week of gains for the S&P 500, which is now up in five of the last six weeks.

● The yield on the 10‐year U.S. Treasury dropped 10 basis points, closing at 1.42%. Meanwhile, the price of a barrel of West Texas Intermediate crude oil rose above $75, hitting its highest level since 2018.

● Economic data continued to suggest solid expansion, with strong manufacturing and consumer confidence reports, as well as solid June jobs data that come in higher than expected, but with moderate wage gains.

Stocks rebound from last week’s fall

The S&P 500 posted another solid week of gains with seven consecutive winning sessions, its longest winning streak since August. For the week, the S&P 500 climbed +1.7% and the tech‐heavy Nasdaq Composite rose nearly +2%. The S&P 500 has now risen in five of the past six weeks, while the Nasdaq has gained in six of the past seven weeks. One weak spot for equities was small caps, as the Russell 2000 Index fell ‐1.2%for the week. The price of a barrel of West Texas Intermediate crude oil rose above $75, hitting its highest level since 2018. Signs of solid economic growth continued with June U.S. manufacturing activity from both ISM and Markit coming in at historically high levels and well into expansion territory. Several major banks announced plans to return capital to shareholders in the form of increased dividends and share buybacks following last week’s successful stress test of the sector by the Fed. But the market was particularly enthused by a solid employment report for June that was released on Friday. June nonfarm payrolls easily topped economists forecast. Factory orders also topped estimates and consumer confidence hit its highest level since February 2020, before the pandemic.

Digits & Did You Knows

FEWER BABIES — Despite a year of lockdowns with our spouses/partners, the number of US births fell in 2020 to 3.6 million, the 12th decline in the last 13 years (source: CDC).

TRAVEL — When travel for vacations slowed in the summer of 2020, rental car companies sold off more than 500,000 rental cars just to survive, leading to a shortage of rental cars and higher prices in 2021 (source: CNN, BTN Research).

(POOL) HELP WANTED — U.S. cities don’t have enough lifeguards, e.g., Austin, TX is short 80% of its 750‐lifeguard goal for the summer of 2021. The pandemic shutdown put a freeze on training and certification programs for lifeguards (source: American Lifeguard Association, BTN Research).

Click here to see the full review.

—

Source: Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange‐traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds may be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐YieldBond(iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 ValueETF);MidGrowth(iSharesRussell Mid‐CapGrowthETF);MidValue (iSharesRussell Mid‐Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4%Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory services offered through Prime Capital Investment Advisors, LLC. (“PCIA”), a Registered Investment Adviser. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).

© 2021 Prime Capital Investment Advisors, 6201 College Blvd., 7th Floor, Overland Park, KS 66211.

that jumped +26.6%. Gains like those, even off the extraordinarily low bases from the depths of last year’s COVID lockdowns, are bound to create inflation concerns. U.S. stocks pulled back more than ‐4% from the May 7th all‐time highs in both the second and third weeks of the month, and VIX volatility spiked to about 28 and 26 on each of those declines. But in the end the bulls took the victory as investors pushed aside the inflation fears in favor of recovery optimism. The S&P 500 rose +0.7% to post its fourth consecutive positive month, and sixth of the past seven. The small‐cap Russell 2000 index, which is more leveraged to the economic reopening, posted its eighth straight positive month for the first time since 1995.

that jumped +26.6%. Gains like those, even off the extraordinarily low bases from the depths of last year’s COVID lockdowns, are bound to create inflation concerns. U.S. stocks pulled back more than ‐4% from the May 7th all‐time highs in both the second and third weeks of the month, and VIX volatility spiked to about 28 and 26 on each of those declines. But in the end the bulls took the victory as investors pushed aside the inflation fears in favor of recovery optimism. The S&P 500 rose +0.7% to post its fourth consecutive positive month, and sixth of the past seven. The small‐cap Russell 2000 index, which is more leveraged to the economic reopening, posted its eighth straight positive month for the first time since 1995. Importantly, vaccination rates in Europe have picked up after a relatively slow start. That has helped Eurozone economic sentiment improve for four straight months and hit its highest level since 2018.The COVID crisis in India has also made much needed progress with over 190 million vaccines so far administered–only behind the totals of US and China. As a result, those economies are also rebounding nicely. As seen in the chart above, both developed and emerging international PMIs are rising and are well into expansion levels (above 50). The MSCI EAFE Index gained +3.3% in May, outperforming U.S. stocks for the first time in 2021.

Importantly, vaccination rates in Europe have picked up after a relatively slow start. That has helped Eurozone economic sentiment improve for four straight months and hit its highest level since 2018.The COVID crisis in India has also made much needed progress with over 190 million vaccines so far administered–only behind the totals of US and China. As a result, those economies are also rebounding nicely. As seen in the chart above, both developed and emerging international PMIs are rising and are well into expansion levels (above 50). The MSCI EAFE Index gained +3.3% in May, outperforming U.S. stocks for the first time in 2021.