Quick Takes

- First Quarter Has Volatile End. Risk assets went on a roller coaster ride for the final month of the quarter with the collapse of multiple banks across the globe.

- Fed Shakes Off Banking Woes, Increased Rates. The Fed implemented increased interest rates by 25bps during the FOMC’s March meeting despite the concerns in the financial services sector. While commentary seemed to leave room for further hikes, market participants began pricing in interest rate cuts as early as later this year. With market interest rates retreating, there was a flurry of real estate activity.

- Greenback Stumbles. With market interest rates tumbling during the month of March, the dollar was dragged down with them. This led to International markets posting respectable results for the month, despite concerns of contagion from the global banking sector.

- Labor Markets and Inflation. While inflation metrics came largely in-line with market expectations, the FOMC expressed concerns with how persistently strong the labor market has remained throughout their tightening cycle. The FOMC also expects tighter lending standards from creditors and expect this to have a similar impact as a hike in interest rates.

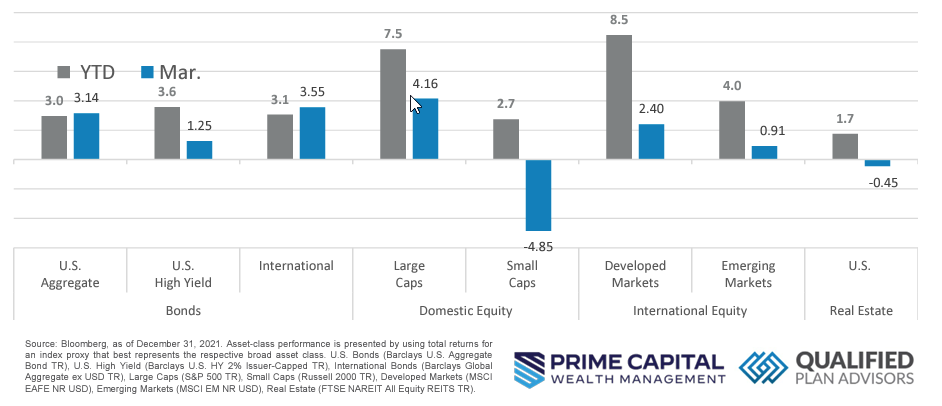

Asset Class Performance

Markets were volatile for the month of March with concerns of fallout from several banks collapsing around the globe. While governments stepped in to stabilize the financial services sector, there was a general flight to safety leading to interest rates falling, bonds performing well, and growth styled equities also posting a strong month of performance.

Markets & Macroeconomics

The month of March gave market participants a flashback to the Great Financial Crisis as several banks collapsed, both domestically and abroad. To alleviate a risk of contagion spreading across the global financial system, governments across the globe stepped in to stabilize the sector, with the FDIC guaranteeing all deposits, even those above the $250,000 maximum, and the Swiss government brokering a sale of Credit Suisse to rival UBS. As market participants were still digesting the risks to the financial sector and the government intervention, the FOMC voted to increase interest rates by 25bps during their March meeting. Regardless of the turmoil in the banking sector, the Fed remained concrete in their fight against inflation with commentary hinting at the possibility of more rate hikes in the future but will be heavily dependent on macroeconomic data readings as well as the continued development within the banking sector. Despite these comments, the bond market diverged from FOMC members’ dot plot, an estimate of where the FOMC see future interest rates, and began to price in rate cuts, not hikes, starting later this year. This divergence illustrates that the market seems to be pricing in more risk than the FOMC is currently seeing and ultimately appears that a majority of market participants are anticipating a recession in the near future. As a result, market participants believe the Fed will be forced to abandon the fight against inflation and begin to stimulate the economy back towards expansion. Because of this viewpoint, interest rates plummeted throughout the month of March.

Bottom Line: Despite the stress in the financial services sector throughout the month of March, the FOMC increased interest rates during their March meeting. While guidance left the door open for more rate hikes in the future, market participants began to price in rate cuts as early as later this year. This means that market participants are anticipating a recession very soon and thus the FOMC will be forced to pivot in their fight against inflation to stimulate the economy to a sufficient level of output to reduce the effects of a contraction in economic production.

Download the full review.

©2023 Prime Capital Investment Advisors, LLC. The views and information contained herein are (1) for informational purposes only, (2) are not to be taken as a recommendation to buy or sell any investment, and (3) should not be construed or acted upon as individualized investment advice. The information contained herein was obtained from sources we believe to be reliable but is not guaranteed as to its accuracy or completeness. Investing involves risk. Investors should be prepared to bear loss, including total loss of principal. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Past performance is no guarantee of comparable future results.

Source: Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange-traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds June be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐Yield Bond (iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 Value ETF); Mid Growth (iShares Russell Mid-Cap Growth ETF); Mid Value (iShares Russell Mid-Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4% Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd., Suite#150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”). Securities offered by Registered Representatives through Private Client Services, Member FINRA/SIPC. PCIA and Private Client Services are separate entities and are not affiliated.

© 2023 Prime Capital Investment Advisors, 6201 College Blvd., Suite #150, Overland Park, KS 66211.

- Alphabet stock pullback a buying opportunity - July 25, 2024

- Prime Capital Investment Advisors Welcomes James Burton as Independent Director of Advisory Board - July 15, 2024

- How Tax Planning Differs For Young Clients - July 15, 2024