The Bottom Line

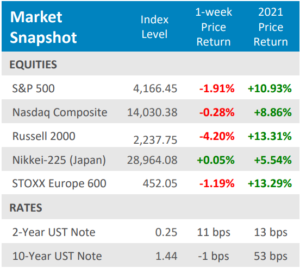

● U.S. equities advanced for the third week in a row and sixth in the last seven. Major U.S. indices closed at record highs, overcoming a big drop on Thursday over fears of the spreading Delta variant and slowing global growth.

● Despite a +7 basis point rally on Friday, the yield on the 10‐year U.S. Treasury dropped ‐6basis points forthe week, closing at 1.36%. At its lowest point on Thursday the 10‐year was down near 1.25%.

● The Labor Department reported that May job openings rose by +16,000, pushing the total to a new record high of 9.2 million jobs, which nearly matches the 9.3 million unemployed Americans that are actively seeking jobs.

2021✔️Friday✔️Record Highs✔️

In what seems to have become a regular occurrence in 2021, major U.S. indices set fresh all‐time highs on Friday, capping an otherwise wobbly week. It took a big rally on Friday to overcome Thursday’s losses over fears of the Delta COVID variant spreading and worries that global growth was peaking. It was the third straight weekly gain for the S&P 500 and the sixth week of gains in the last seven. The Dow Jones Industrial Average and Nasdaq Composite also finished at record highs. Though small caps fell short of record highs, falling ‐1.1% for the week, the Russell 2000 did rebound+2.0% on Friday. The Friday stock rally was spurred by news that Pfizer is working on a booster shot to combat the Delta variant and China’s central bank was boosting liquidity by reducing the amount of cash its banks must hold in reserve. The yield on 10‐year U.S. Treasury has fallen for two consecutive weeks, and fell as low as 1.25% on Thursday, but reversed noticeably on Friday. The 10‐year Treasury yield rose 7 basis points Friday to close at 1.36%. Economic news was relatively quiet during the week and markets appeared to shrug an executive order by President Joe Biden’s to crack down on anticompetitive practices among U.S. businesses.

Digits & Did You Knows

CANCER — The diagnoses of some forms of cancer fell by more than ‐50% in 2020 when compared to 2019, not because cancer is on the decline but because 94% of Americans postponed their annual screenings and many cancer clinics suspended the collection of biopsies (source: Propublica, BTN Research).

REAL ESTATE — In March 2020 1.49 million existing homes were on the market for sale. By March 2021, just 1.05 million homes were on the market. With a smaller supply, home prices soared. The median sales price of existing homes sold rose from $280,700 in March 2020 to $350,300 in May 2021, a +25% increase (source: Nat’l Association of Realtors, BTN).

Click here to see the full review.

—

Source: Bloomberg. Asset‐class performance is presented by using market returns from an exchange‐traded fund (ETF) proxy that best represents its respective broad asset class. Returns shown are net of fund fees for and do not necessarily represent performance of specific mutual funds and/or exchange‐traded funds recommended by the Prime Capital Investment Advisors. The performance of those funds may be substantially different than the performance of the broad asset classes and to proxy ETFs represented here. U.S. Bonds (iShares Core U.S. Aggregate Bond ETF); High‐YieldBond(iShares iBoxx $ High Yield Corporate Bond ETF); Intl Bonds (SPDR® Bloomberg Barclays International Corporate Bond ETF); Large Growth (iShares Russell 1000 Growth ETF); Large Value (iShares Russell 1000 ValueETF);MidGrowth(iSharesRussell Mid‐CapGrowthETF);MidValue (iSharesRussell Mid‐Cap Value ETF); Small Growth (iShares Russell 2000 Growth ETF); Small Value (iShares Russell 2000 Value ETF); Intl Equity (iShares MSCI EAFE ETF); Emg Markets (iShares MSCI Emerging Markets ETF); and Real Estate (iShares U.S. Real Estate ETF). The return displayed as “Allocation” is a weighted average of the ETF proxies shown as represented by: 30% U.S. Bonds, 5% International Bonds, 5% High Yield Bonds, 10% Large Growth, 10% Large Value, 4% Mid Growth, 4%Mid Value, 2% Small Growth, 2% Small Value, 18% International Stock, 7% Emerging Markets, 3% Real Estate.

Advisory services offered through Prime Capital Investment Advisors, LLC. (“PCIA”), a Registered Investment Adviser. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).

© 2021 Prime Capital Investment Advisors, 6201 College Blvd., 7th Floor, Overland Park, KS 66211.

that jumped +26.6%. Gains like those, even off the extraordinarily low bases from the depths of last year’s COVID lockdowns, are bound to create inflation concerns. U.S. stocks pulled back more than ‐4% from the May 7th all‐time highs in both the second and third weeks of the month, and VIX volatility spiked to about 28 and 26 on each of those declines. But in the end the bulls took the victory as investors pushed aside the inflation fears in favor of recovery optimism. The S&P 500 rose +0.7% to post its fourth consecutive positive month, and sixth of the past seven. The small‐cap Russell 2000 index, which is more leveraged to the economic reopening, posted its eighth straight positive month for the first time since 1995.

that jumped +26.6%. Gains like those, even off the extraordinarily low bases from the depths of last year’s COVID lockdowns, are bound to create inflation concerns. U.S. stocks pulled back more than ‐4% from the May 7th all‐time highs in both the second and third weeks of the month, and VIX volatility spiked to about 28 and 26 on each of those declines. But in the end the bulls took the victory as investors pushed aside the inflation fears in favor of recovery optimism. The S&P 500 rose +0.7% to post its fourth consecutive positive month, and sixth of the past seven. The small‐cap Russell 2000 index, which is more leveraged to the economic reopening, posted its eighth straight positive month for the first time since 1995. Importantly, vaccination rates in Europe have picked up after a relatively slow start. That has helped Eurozone economic sentiment improve for four straight months and hit its highest level since 2018.The COVID crisis in India has also made much needed progress with over 190 million vaccines so far administered–only behind the totals of US and China. As a result, those economies are also rebounding nicely. As seen in the chart above, both developed and emerging international PMIs are rising and are well into expansion levels (above 50). The MSCI EAFE Index gained +3.3% in May, outperforming U.S. stocks for the first time in 2021.

Importantly, vaccination rates in Europe have picked up after a relatively slow start. That has helped Eurozone economic sentiment improve for four straight months and hit its highest level since 2018.The COVID crisis in India has also made much needed progress with over 190 million vaccines so far administered–only behind the totals of US and China. As a result, those economies are also rebounding nicely. As seen in the chart above, both developed and emerging international PMIs are rising and are well into expansion levels (above 50). The MSCI EAFE Index gained +3.3% in May, outperforming U.S. stocks for the first time in 2021.